If money feels gone the moment it arrives, you’re not alone. A lot of people who work hard every week still end up doing mental math at the grocery store, delaying purchases, or hoping the next deposit lands before the next bill hits.

The good news is that budgeting on a tight income is not about perfection. It’s about creating a system that helps you stay afloat, reduce stress, and slowly build breathing room. How to budget when you live paycheck to paycheck starts with one simple idea, you need a plan that works with real life, not an idealized version of it.

Start With Survival, Not Perfection

When cash is tight, the first goal is not saving 20 percent of your income. The first goal is making sure the essentials are covered and the rest is assigned on purpose.

List your non-negotiables first

Write down the expenses that keep life moving:

- Rent or mortgage

- Utilities

- Groceries

- Transportation

- Minimum debt payments

- Childcare or pet care if applicable

- Insurance and prescriptions

This gives you a clear picture of what must be paid before anything else. If you like structure, a simple budget can help you see where money is leaking each month.

Track every dollar for one month

For 30 days, write down every expense, even the small ones. Coffee, delivery fees, app subscriptions, and convenience store stops matter more than people think when income is tight.

You do not need fancy software. A notes app, notebook, or spreadsheet is enough. The point is to find patterns, not judge yourself.

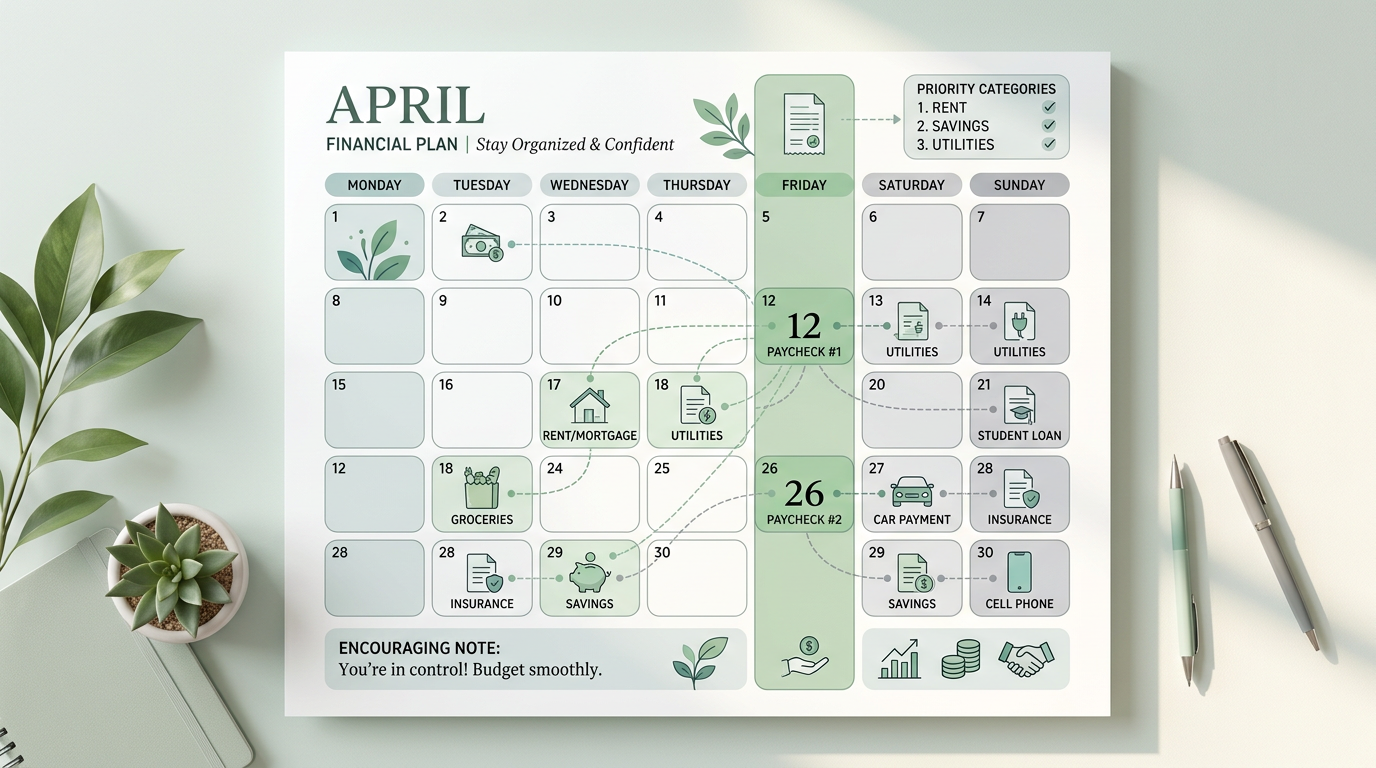

Use a Paycheck-Based Budget

When you live paycheck to paycheck, monthly budgeting can feel too vague. A paycheck-based plan is usually easier because it matches the way money actually arrives.

Assign each paycheck a job

Before each payday, decide where that money will go. A practical order looks like this:

- Rent and utilities

- Food and transportation

- Minimum debt payments

- Insurance and essential bills

- Small buffer for irregular expenses

If a bill is due before your next paycheck, that expense gets priority. This reduces the panic of wondering what gets paid first.

Split bills by due date, not by category only

A common mistake is budgeting by month without thinking about timing. If your rent is due on the first and your paycheck lands on the fifth, you need a short-term plan to bridge that gap.

That might mean:

- Changing due dates when possible

- Keeping a small bill cushion

- Saving part of one paycheck for the next cycle

This is one of the most effective answers to how to budget when you live paycheck to paycheck, because timing matters as much as totals.

Cut Costs Without Making Life Miserable

Cutting costs does not mean living on rice and regret. It means trimming the expenses that give you little value.

Look for the quiet money drains

Start with the small recurring costs that add up:

- Streaming subscriptions you rarely use

- Delivery charges and convenience fees

- Bank overdrafts and late fees

- Impulse shopping

- Extra data plans or unused memberships

Even reducing a few of these can free up money for food, gas, or savings.

Use the 48-hour pause rule

If you want to buy something nonessential, wait 48 hours. This helps you separate emotional spending from actual need.

For many people, that pause alone can stop a lot of budget damage.

Build a Tiny Emergency Buffer

A full emergency fund may feel impossible right now, and that’s okay. Start smaller.

Aim for your first $100 to $500

Your first emergency cushion does not need to be huge. It just needs to help with the most common surprises, such as:

- A prescription refill

- A car repair

- A broken phone charger or tire

- An unplanned school or pet expense

Keep this money separate if possible, even if it’s in a basic savings account.

Automate a small transfer

If your budget allows it, move a tiny amount every payday, even $10 or $20. Small automatic transfers work because they remove the decision-making pressure.

The goal is momentum. Once you prove to yourself that saving is possible, it becomes easier to keep going.

Protect Your Budget From Irregular Expenses

One reason people feel stuck is that they budget for the obvious bills but forget the irregular ones.

Make room for the things that show up later

These expenses often sneak up:

- Car maintenance

- Holiday gifts

- Annual fees

- Pet vaccinations

- School supplies

- Clothing replacements

Create a “sinking fund” for these costs by setting aside a little each paycheck. That way, one surprise does not wreck the whole month.

Use separate buckets if that helps

Some people like one checking account with separate notes. Others use multiple savings buckets. Use whatever keeps the categories clear and reduces overspending.

Increase Flexibility Wherever You Can

If your income changes from week to week, flexibility matters even more than precision.

Plan for a low-income version of the month

Budget as if your next paycheck may be smaller than expected. If extra money comes in, use it to catch up, save, or pay down debt.

That approach keeps you safer when hours get cut or work is irregular.

Negotiate when possible

You can sometimes lower pressure by asking for:

- A due date change

- A payment plan

- A lower interest rate

- Reduced internet or phone costs

- A different insurance payment schedule

A five-minute phone call can sometimes save real money.

Keep Motivation Realistic

Budgeting while stretched thin is emotionally tiring. You are not failing because progress feels slow.

Measure wins that are not just savings

Success might look like:

- Paying all essentials on time

- Avoiding overdraft fees

- Cutting one subscription

- Building a $200 buffer

- Reducing credit card use

These are real wins. They matter.

Expect setbacks and reset quickly

One unexpected expense does not ruin your budget. The key is to restart with the next paycheck instead of giving up.

Budgeting is not a perfect streak. It is a habit of returning to the plan.

FAQ

What is the best budget method for paycheck to paycheck living?

A paycheck-based budget is usually the easiest because it matches when money actually arrives. It helps you assign each paycheck to specific bills and essentials before spending on extras.

Should I save money if I barely get by?

Yes, but start very small. Even a tiny emergency fund can keep one surprise expense from turning into debt or overdraft fees.

How do I stop overspending when money feels stressful?

Use a pause rule, remove saved payment cards from shopping apps, and give yourself a small allowed amount for treats. Stress spending is easier to control when you make it harder to do automatically.

What if my income changes every week?

Budget from your lowest predictable income, then treat extra money as a bonus for catch-up, debt, or savings. That keeps your plan safer during slow weeks.

Is it okay to use cash envelopes?

Yes. Cash envelopes work well for categories like groceries, gas, or personal spending because they create a hard limit. If cash is inconvenient, digital buckets can do something similar.

How do I budget when bills are due before payday?

First, ask whether any due dates can be changed. If not, build a small buffer over time or split the bill into weekly amounts so the next paycheck is already partly reserved.

Keep Your Budget Simple Enough to Follow

The best budget is the one you can actually use every week. If your system is too complicated, it will collapse the moment life gets busy.

Focus on three things, what you owe, what you must keep, and what you can trim. Then give every paycheck a purpose before it disappears.

Your next step

Choose one action today, track spending, list your fixed bills, or set up a tiny automatic savings transfer. If you want more practical money advice, visit Content Beast for more helpful guides built for real life.

Conclusion

Learning how to budget when you live paycheck to paycheck is less about restricting every dollar and more about giving your money a clear job. When you track spending, prioritize essentials, plan by paycheck, and build even a small buffer, you create stability one step at a time.

You do not need a perfect system to make progress. You just need one that helps you stay in control, reduce stress, and keep moving forward.